Marklin Johnson drove to the grocery store with her boyfriend and 5-month-old son in March 2025. They needed groceries and a warm indoor diversion on a cold Connecticut winter day.

As they were paying at the register, Johnson looked out the window and noticed her car was gone.

“I didn’t know what to do,” Johnson said. “I didn’t know what to say or who to call.”

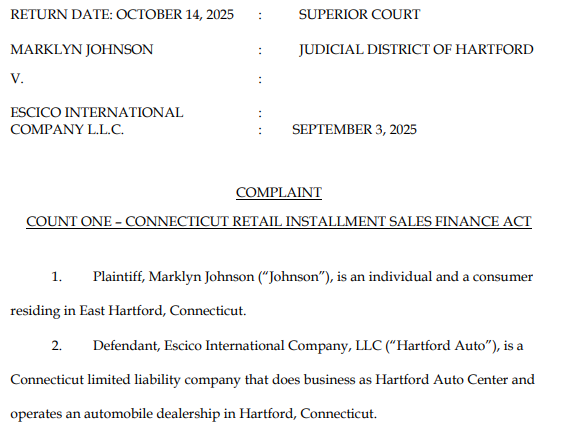

Johnson’s legal complaint in Superior Court in Hartford reveals that the used car dealership that sold her the car two months ago decided to repossess it at an extremely inopportune time, even though she had never missed a payment.

Unfortunately, Mr. Johnson’s story is one of many. Bankrate spoke with consumer protection attorneys in five states who represent clients in similar ongoing litigation. One lawyer called them “rampant.” Sometimes it’s not just a repossession, especially when a dealer or their auto financing partner reports the car as stolen to the police if the consumer doesn’t return it promptly.

California-based attorney Sparky Abraham said one of his clients never expected a car repossession story to end in handcuffs.

“I can’t say much because I haven’t gotten to the latest (case) situation yet,” Abraham said. “But I’ll tell you,[my client]had a video of herself being arrested and they had a gun pointed in her face like they were buying a car. You know what?”

Like that woman, what happened to Johnson began as a simple “yo-yo loan.” Her dealer guaranteed loan approval, and five days after the sale was “closed,” they started texting and calling her to tell her it had fallen through. She was given options before foreclosure. Either return the car or succumb to less attractive loan terms.

When faced with a problem, most consumers want the car they’re already driving and “eat the difference and sign a new contract,” said Kansas City consumer attorney Bryce Bell. Other consumers simply are not aware of their legal rights. This means that only a small percentage of these bait-and-switch cases actually result in litigation.

As part of Bankrate’s ongoing efforts to expose predatory financial practices, Yo-Yo Finance seems worthy of attention.

Prime Minister Johnson: ‘I wasn’t prepared for what happened next’

Johnson, 23, and her 14-month-old son needed a car for the same reason we all need wheels. Going to and from doctor’s appointments, work, etc. So, tired of borrowing his parents’ car, Johnson looked for something affordable and zeroed in on a 2017 Acura ILX listed by Hartford Auto for $13,999. The used car dealer claimed to offer “guaranteed” approval, but asked Johnson to increase her down payment from $1,500 to $3,200 in order to close the deal, according to the complaint.

“I knew it was my name and I had just bought it and it was ‘new,’ so I didn’t have any problems with it. I was so excited,” said Johnson, who is currently pursuing a career as a nurse. “Then I found out my baby had a car and everything fell into place.”

Things fell apart about five days after she drove the Acura out of the parking lot. The complaint says he received text messages and phone calls from the dealer stating that “(financing partner) Winthrop Financial was having trouble accepting the loan and new loan documents would need to be signed.”

“I’m not going to lie…I was really heartbroken,” Johnson recalled. “I had already signed the contract, I had already done what I had to do…I was not prepared for what happened next.”

Related: The number of car pickups increased by 43%. If this happens, here’s what to do

Two months later, Johnson found herself in a grocery store parking lot with no car at all, and her immediate concern was how to get home. She remembers an Uber driver allowing her toddler into the car without a car seat base.

It remained in the Acura that had just been towed away.

Read Mr. Johnson’s full legal complaint.

Yo-yo financing through unilateral car purchase contract

That’s what yo-yo finance is all about. Imagine yourself experiencing the highs of being evicted from the property, perhaps to increase your down payment or face higher interest rates, and the lows of perhaps being called back. In the intervening days, you may have been showing off your new vehicle to family and friends, or flipping your budget to make the math work.

“It’s hard for someone to say, ‘No, I’m not going to pay another $2,000 for the down payment or whatever the (dealer) demands,'” says John Van Alst, principal attorney at the National Consumer Law Center (NCLC), when they’re really invested. “Sometimes, in the most egregious cases, this is done as a technique.[Dealers]don’t even check with the other finance company they are assigning the retail installment sales contract to. They simply do this as a way to get them to agree to more onerous terms.”

Believe it or not, yo-yo financing itself (prior to renegotiation or foreclosure) is perfectly legal because each state gives dealers a certain number of days to close the loan after the buyer signs the documents. For example, in Washington it’s 4 days, but in California it’s 10 days. If the dealer is unable to secure financing, he or she may cancel the contract within that period.

This is despite NCLC and the National Association of Consumer Advocates (NACA) lobbying the FTC for simplicity and uniformity.

“It doesn’t even need to be highly regulated,” agreed Kristin Hines, NACA’s senior policy director. “It just means that the contract is the final contract. There shouldn’t be terms in there that harm the consumer…because the dealer doesn’t know how to do a deal.”

Yo-yo financing, also known as bush fraud or spot delivery fraud, can be even more troublesome for buyers who are trading in an older model to buy a new car. In these cases, the dealer may sell your trade-in before you can call back to renegotiate your loan.

Bankrate reported on the fact that auto dealers have been exempt from federal oversight since the Consumer Financial Protection Bureau’s inception. The CFPB’s recent sidelines have little to do with that. There’s also the fact that where you live determines how protected you are from auto retail fraud. Regulators in your state may be more enthusiastic than others.

Related: Predatory auto loans are legal, but some dealers offer auto loans to uninformed consumers.

But another unfortunate reality is that yo-yo financing appears to be occurring nationwide. And it’s equally disconcerting for the professionals who litigate these cases every day. Mr. Bell, a Missouri-based attorney, wonders why buying a car seems to be the only transaction in which the seller can change his mind after the contract is signed.

“If you’re an honest dealer and an honest business, why wouldn’t you want that deal to close for the consumer?” Bell asks.

Just like anything else in life, follow your incentives, Bell adds. Car salesmen can push the envelope when they are incentivized, perhaps by a commission, to get buyers to vacate space in their cars. And without federal regulation (or enforcement), dealers are free to make these mistakes (or in some cases malicious acts).

How dealers deal with yo-yo loan failure cases like Johnson’s, and how law enforcement deals with the aftermath, also depends on where you live. But your police department may be more important than your state. Abraham, the California attorney, said he has worked on two cases in Southern California that involved nearby police departments. One police station treated it as a civil dispute, while another acted as if it were a criminal case and arrested the car’s purchaser.

“This is the neighboring jurisdiction, right?” Abraham says. “This is Anaheim Police Department, Pomona Police Department. These are Los Angeles Police Department and Beverly Hills Police Department, right?”

And if the dealer reports the car as stolen, like Hartford Auto found Johnson’s Acura at Aldi, likely because it’s not as easy to find as Hartford Auto found Johnson’s Acura at Aldi, and given the car’s value, the buyer could face felony-level charges.

What would you do if you were in Johnson’s shoes?

Get everything in writing. That’s the go-to advice from consumer protection lawyers interviewed by Bankrate. That way, you’ll have a record of what the dealer did and when, and you can prove that financing your yo-yo led to legal but illegal activity.

In Ms. Johnson’s case, her complaint alleges that Hartford Auto violated Connecticut law by failing to provide pre- or post-recovery notice, including, for example, a 60-day right to retrieve her personal property, such as the base of her son’s car seat. Similarly, the company did not share its intention to resell Acura (it did so last August). The complaint also says Hartford Auto violated the Connecticut Unfair Trade Practices Act by, among other things, falsely representing that the loan to Mr. Johnson could and had been approved. She was unable to recover her $3,200 down payment, but is now seeking more than $15,000 in damages and attorney fees.

Seeking legal assistance is also a smart move, especially if you need help understanding your rights. Please note that you may not always get a reassuring response. For example, Abraham received a phone call from a prospective customer relaying a common threat from dealers. Please return the car or I will call the police.

“My advice is: ‘Look, it (may be) illegal for them to do that. They may still be doing it, and if they are, you can call me and maybe sue me, you can sue for damages, but your life will probably be better off if you just focus on (returning) the car,” he says.

It’s also wise to file complaints with the CFPB, FTC (even if they don’t listen), and your state’s consumer protection bureau. At the very least, it creates a record of experiences that can lead to broader and more meaningful change.

As for Johnson, his first car-buying experience certainly left a “bad impression.” If she could do it all over again, she would do everything in her power to budget and save for a car, avoiding any kind of debt or scams from car dealers.

“If I could go back in time,” she says, “I would be happy. “I probably would have just waited, feeling like a burden to[my parents]to save up the money to buy a car that I could buy outright, a car that I could call my own at the end of the day.”